Profit First Changed My Financial Life (And My Tax Season)

TL;DR

- Two books changed how I think about money: Profit First (automate business finances) and I Will Teach You To Be Rich (automate personal finances). Together they cover everything.

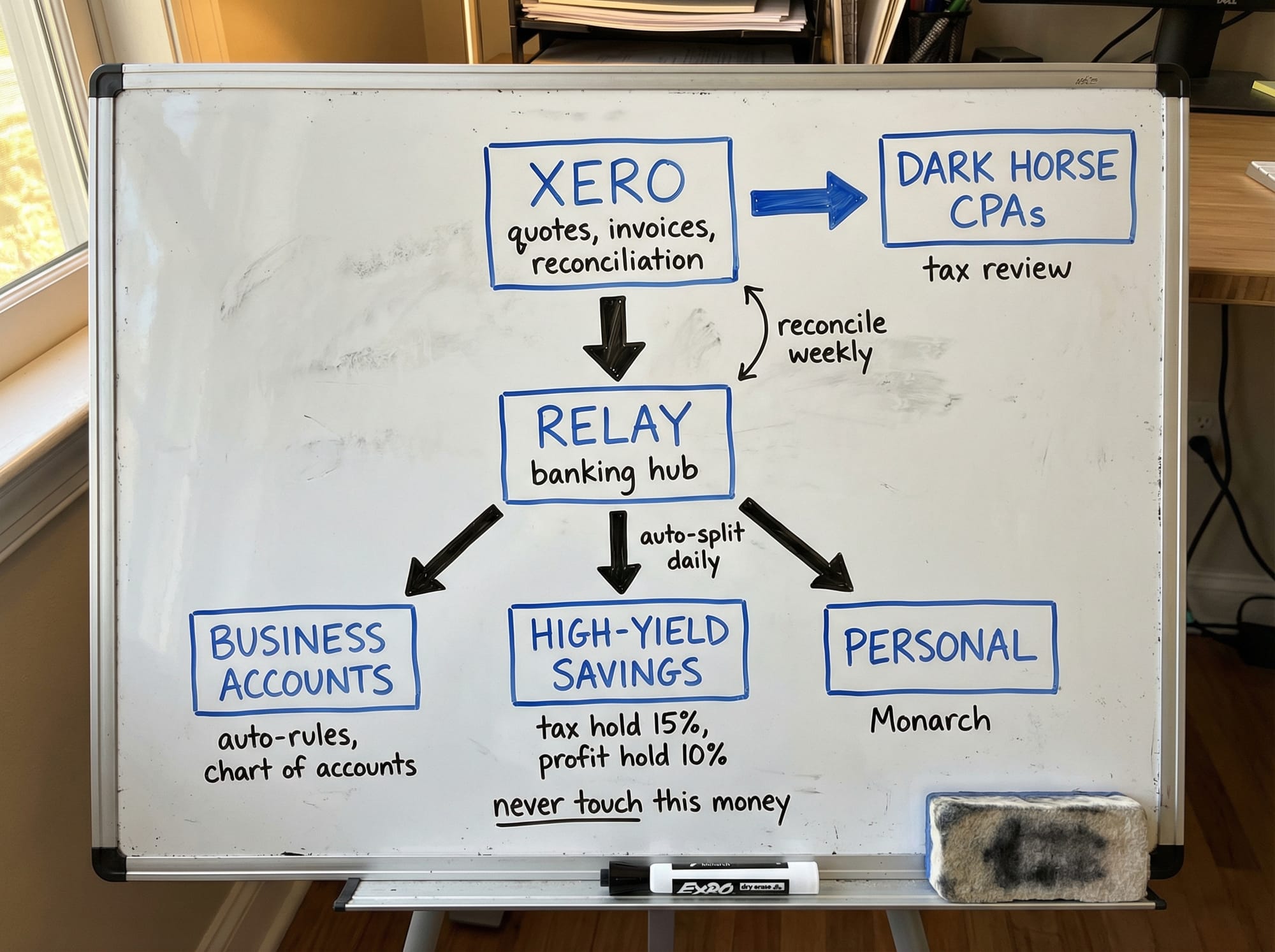

- My stack: Relay Financial (banking + daily auto-transfers), Xero (accounting), Dark Horse CPAs (Xero-native CPA), high-yield savings at a separate bank for tax holds and profit.

- I did my tax prep this year in about an hour from a pool in Arizona. Not because I'm special. Because the system does the work.

- The real payoff: money stops being the thing that keeps you up at night and becomes a game you can actually play.

- Tools I'm watching: Kick (self-driving bookkeeping), Digits (AI-native accounting, Xero co-founder joined).

I got my tax projection back from my CPA last week. I had more than enough set aside to cover it. All of my reconciliations were current. My tax prep took about an hour, and I did it sitting by a pool in Arizona.

Three years ago I was the guy googling "can I file an extension" at midnight, scrolling through six months of bank statements trying to figure out what a $347 charge in August was.

The difference is the system.

My financial life has been a roller coaster. I've run businesses across multiple countries. Different bank accounts, different currencies, different tax systems. I've paid penalties. There were years where money felt like it was suffocating me, and years where everything clicked. The suffocating part always came with a blindside. But I figured it out every time and got back up.

Here's the system I built after years of getting it wrong.

Tax prep from a pool in Arizona. The system makes this possible.

The two books that changed everything

I read Ramit Sethi's I Will Teach You To Be Rich in high school. The core idea stuck with me for years: automate your finances so the right things happen without you thinking about it. Pay yourself first. Set up the accounts. Let the money flow where it needs to go.

I understood the concept. I just couldn't execute it for my business.

Then I read Profit First by Mike Michalowicz, and it was the first time something about business finances actually made sense to me.

The idea: every dollar that comes into your business gets bucketed automatically into separate accounts. Not one big checking account where you guess what's available. Separate accounts for operating expenses, taxes, profit, and owner's pay. The system decides the allocation, not you. You set the percentages once, based on your revenue level and industry benchmarks, and then you let it run.

Ramit handles personal finances. Profit First handles business finances. Together they cover everything.

The Profit First concept: every dollar gets bucketed. Income splits automatically into Expenses, Taxes, Profit, and Owner's Pay.

The three types of self-employed people at tax time

If you're self-employed, you're one of three people right now.

The panicking freelancer. You haven't reconciled anything since last summer. You're staring at a pile of 1099s and wondering if you should just do TurboTax yourself or bite the bullet and find a CPA two weeks before the deadline. You know you should have been tracking things all year. You didn't. Now it's a weekend of pain.

The delegating founder. You hired a CPA. Maybe even a bookkeeper. You think you're covered. But if I asked you right now what your effective tax rate is, or how much cash you actually have after obligations, you'd have to text your accountant and wait. That's not delegation. That's abdication. You've outsourced the one thing you should understand better than anyone: where your money goes.

The person with their finances dialed. Reconciliations current. Tax holds funded. You know your numbers because you built a system, not because you crammed last week. If this is you, I want your stack.

I was person one for years. Then person two. I thought hiring a CPA meant I was being responsible. It didn't. It meant I was paying someone to manage something I didn't understand, and hoping it worked out.

I had to lean hard on the people and systems I had in place. I didn't always get it right. I was stuck between knowing what good looked like and not being able to execute it yet. For a long time.

My exact stack

This is what I actually use. Not what I'd recommend in theory. What I run every day.

Relay Financial for banking. Only bank I've found that's built specifically for Profit First. You create multiple checking accounts (I have separate ones for income, operating expenses, tax, profit, and owner's pay) and set up auto-transfer rules. Every day, Relay disperses money from my income account into the right buckets based on the percentages I set.

The tax hold and profit accounts transfer automatically to a high-yield savings account at a completely separate bank. I don't see that money in my daily banking. That's the entire point. If you can see it, you'll spend it.

Xero for accounting. I've used Xero for over six years. Started when I was living in South Africa, where it's the default. When I moved back to the US, every accountant told me I had to switch to QuickBooks Online. So I tried. For one year.

Worst financial experience of my life. I couldn't tell what was happening with my money inside QBO. The interface felt designed by committee. Categorization was a mess. Reports didn't make sense to me. I know millions of businesses run on QuickBooks, and plenty of people love it. For me, Xero is the tool that lets me actually understand my money, and that understanding is the entire point. I went back and never looked back.

Sean Winkel at Dark Horse CPAs for tax strategy and accounting. Finding a Xero-native CPA in the United States is hard. Most accounting firms are QuickBooks shops. Dark Horse is one of the few that works natively in Xero. Sean handles my tax optimization strategy, and because my books are clean year-round, our conversations are 30 minutes instead of three-hour panic sessions.

On the personal side, I use Monarch for budgeting so I can see the full picture across business and personal. Business being clean doesn't matter if you can't see the whole thing.

My financial stack mapped out. Income flows through Relay, gets tracked in Xero, reviewed by Dark Horse CPAs. Monarch handles the personal side.

How it works in practice

The daily flow:

- Revenue hits my Relay income account.

- Relay's auto-transfer rules fire daily. They split the money by percentage into operating expenses, tax hold, profit, and owner's pay accounts.

- The tax hold and profit amounts transfer out to the high-yield savings account at the separate bank.

- I pay business expenses from the operating expenses account. That's the only account I "spend" from.

- Xero syncs with all of these accounts and categorizes transactions. Bank rules handle most of the recurring stuff automatically.

- I do a quick reconciliation check in Xero once or twice a month. Takes maybe 15 minutes because there's almost nothing to catch up on.

When tax time comes, I open Xero, export what Sean needs, and we're done. An hour. By a pool. In Arizona.

The whole point is that the system removes decisions. The percentage decides how much goes to taxes. The auto-transfer moves profit before I can touch it. Bank rules handle 90% of categorization. I'm not disciplined. I just built a system that doesn't require discipline.

Side note: figuring out your Profit First percentages is way easier now than when I started. The book gives you starting percentages, but you can dial them in with a quick AI conversation about your revenue level, industry, and goals. Takes 10 minutes.

What happens when the system runs

Here's the part nobody talks about.

Once the constraints are baked in and the system runs without you thinking about it, money stops being the thing that wakes you up at 3 AM. It becomes a game. Once your financial data is actually clean, the questions you can start asking get really interesting.

I can look at my social media engagement numbers alongside my revenue and actually see whether a LinkedIn series drove inbound leads or just likes. I can pull up my cost of goods across all four businesses and spot where I'm overpaying for something that could be automated or outsourced. Last quarter I was considering a major annual subscription for a tool that would change how I run client projects. Instead of guessing whether I could afford it, I built a quick forecast model, plugged in my actual numbers from Xero, and could see exactly what that decision looked like over 6 and 12 months. I said yes because the data made it obvious. A year ago I would have agonized over it or just said no to be safe.

That's the game. Not reckless spending. Not gut decisions. The opposite. You know the guardrails exist, so now you can actually experiment. Say no to a client that doesn't fit because you can see your pipeline. Test a pricing model because you know your margins. Take on a risky project because you can model the downside.

I spent years reactive. Now I can step back and see the whole picture. That's where the good decisions actually happen.

Once the system runs, you stop fighting fires and start making decisions from clarity.

A few more examples of what becomes possible:

Seasonal patterns. With a couple years of clean data, you can see which months are lean and pre-load your profit distributions accordingly. No more December panic.

Client profitability. Which clients generate the most revenue per hour of your time? I found one client that was taking 3x the hours for half the margin. Fired them. Revenue went up because I had the capacity for better work.

Runway math. I know exactly how many months I can operate with zero new revenue. That number changes how you negotiate, how you price, and how you sleep.

Tax optimization timing. When your books are current, you can strategically accelerate or defer expenses across quarters. Sean and I have these conversations in real time instead of scrambling in April.

Tools I'm watching

The accounting and bookkeeping space is about to get interesting. A few things on my radar:

Kick -- self-driving bookkeeping. This is the one I'm most excited about. Free for businesses under $25K in expenses. AI categorizes transactions, finds write-offs, matches receipts. Accounting firms using Kick report cutting their monthly close from 15 days to under 24 hours. Reviews say it's 500x more user-friendly than QBO. I haven't switched yet, but I'm watching it closely.

Digits -- AI-native accounting. This one is interesting because Craig Walker, co-founder of Xero, joined the team. They call it an "autonomous general ledger." Trained on $825 billion in SMB transactions. $100/month. If anyone is going to build the next-generation Xero, it might be the people who built the original one.

Where to start

If you're person one or two from the archetypes above, here's your weekend:

- Read Profit First by Mike Michalowicz. It's a weekend read and it's the one that made everything click for me.

- Read I Will Teach You To Be Rich by Ramit Sethi for the personal finance automation side. (Both of these made my list of books every entrepreneur should read.)

- Open a Relay Financial account and set up your Profit First buckets.

- Find a CPA who works in your accounting tool of choice, not the other way around. (Dark Horse CPAs if you use Xero.)

If you want help setting up the system or figuring out your percentages, DM me on LinkedIn. I've done this enough times now that I can walk you through it in 30 minutes.

The goal is getting to the point where you can step back, see the whole picture, and make decisions from clarity instead of panic.

Share & Subscribe

Know a freelancer or founder who dreads tax season? Forward this to them. The system takes a weekend to set up and changes every tax season after it.

Share on LinkedIn · Share on X

This is Automate With Rob, a newsletter about building with AI tools without losing your mind. If someone forwarded this to you, subscribe here.